EVs, batteries, and data centers: The Transformation of Thailand's Eastern Economic Corridor

From Japanese automotive estates to Chinese EV factories and hyperscale data centers, the Eastern Seaboard is being transformed into a launching pad for Chinese EV, battery, and AI ambitions

On a recent visit to Thailand’s industrial heartland of Chongburi, Somnuck Jongmeewasin, research director at EEC Watch and a process engineer by training, describes how the construction of a new hyperscale data center is damaging the delicate coastal mangrove forest of Khlong Tamru in Chonburi.

“The water temperature is affected by the release of water from the DC cooling,” he told me. “This can kill off sea life in the area quickly. I am a former engineer — you can’t fool me with these things.”

For ten years, Somnuck has brought attention to the environmental problems of the Eastern Economic Corridor, a flagship initiative of Thailand’s Junta government under Prayuth Chan-Ocha to spur new investment into Thailand’s industrial heartland, which was originally developed around Japanese infrastructure assistance and auto investment in the 1980s. In the early 1980s, the Japanese government — through JICA and a constellation of private automotive and petrochemical firms — financed and designed the Eastern Seaboard Development Programme, one of the largest aid-funded industrial infrastructure projects in Southeast Asian history. The design followed a deliberate two-zone spatial logic: heavy petrochemical industry concentrated at Map Ta Phut in Rayong; automotive and electronics assembly anchored in Chonburi at the Amata City and later Amata Nakorn estates. Water infrastructure, power distribution, road connections, and the deep-water port at Laem Chabang were engineered specifically to support these two zones and their resource needs.

The Eastern Seaboard became the heart of Thailand’s automotive export industry, hosting Toyota, Honda, Isuzu, Mitsubishi, and a deep Japanese-dominated supply chain. By the 2000s, Thailand was producing over a million vehicles annually — nearly all assembled in or near what is now the EEC. The infrastructure built for that industry persists as a fixed spatial inheritance. Reliable high-voltage power, a deep-water container port, industrial-grade water supply, and flat, large-footprint serviced land are what automotive manufacturing requires. They are also, with minimal modification, ideal for what EV assembly plants and hyperscale data centers require. Chinese capital arriving in the EEC is not creating infrastructure from scratch but rather layering onto an existing infrastructural landscape.

The Prayut government’s plan for the EEC called for seven new tech clusters, a high-speed rail link with Bangkok and its airports, and a new aerotropolis at U-Tapao in Rayong. None of these signature initiatives have born much fruit so far. But in recent years, the FDI from Chinese batteries and EV manufacturing has begun to transform the area.

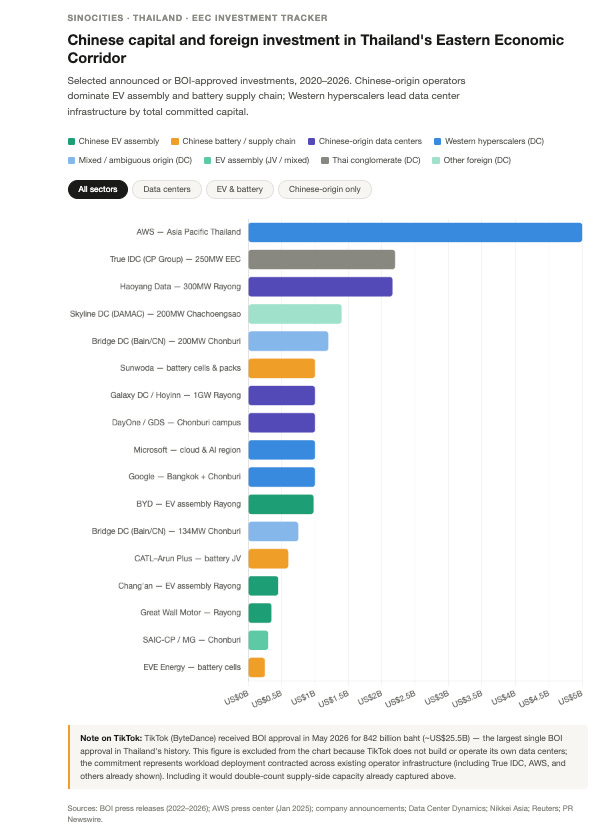

Click for Interactive Chart

Electric vehicles: occupying the Japanese footprint

The most consequential Chinese investment in the EEC — measured by capital committed, employment, and spatial impact — is in electric vehicles and batteries,. Between 2022 and 2025, at least five Chinese automotive brands secured BOI approval for assembly operations in the EEC, with collective announced capacity exceeding 600,000 units per year. The spatial pattern is telling: nearly all of them have located in the EEC, the area that Japanese automotive investment transformed into the so-called Detroit of the East. So far, the area is not going the route of Detroit in de-industrializing, but rather transforming from the diesel era to the EV era.

Great Wall Motor arrived first. In 2020, as domestic Chinese market competition intensified, GWM acquired a mothballed General Motors assembly plant in Rayong — a facility that GM had built during the high point of Japanese-era automotive expansion and abandoned in the 2010s. GWM converted it for its ORA and Haval electric and hybrid lines, with capacity around 80,000 units per year. The symbolism is pointed: a Chinese OEM inheriting the physical shell of an American plant, on land serviced by Japanese-funded infrastructure, to produce EVs for a Southeast Asian market.

BYD 比亚迪 followed with even greater ambition. Having secured BOI approval in 2022, BYD commenced construction at WHA Eastern Seaboard Industrial Estate 36 in Rayong and opened in 2024, with a designed capacity of 150,000 vehicles per year. The facility is BYD’s first overseas assembly plant in Southeast Asia and is positioned as the export hub for the ASEAN market. Chang’an Automobile 长安汽车 has received BOI approval for a comparable 100,000-unit facility in Rayong. Chery, another Chinese OEM with significant export ambitions, is also BOI-approved for EEC production. SAIC-CP, a joint venture between China’s SAIC Motor and CP Group, has operated MG brand vehicles in Thailand for over a decade through a Thai-Chinese partnership structure that insulates the investment from straightforward classification as either foreign or domestic.

Batteries: the deeper supply chain integration

The more structurally significant dimension of Chinese industrial investment in the EEC is not vehicle assembly but battery and energy storage supply chain. Vehicle assembly can be relocated; battery manufacturing, once established, creates deeper dependencies through materials sourcing, technical workforce, and capital intensity.

CATL(宁德时代) the world’s largest EV battery manufacturer, has structured its Thai entry through a joint venture with Arun Plus, a subsidiary of PTT (Thailand’s state-owned petroleum company). The JV model is significant: it mirrors CATL’s approach in other markets of partnering with established state-linked entities to manage regulatory and political risk, while gaining access to land, grid connections, and import exemptions that independent foreign investment cannot easily obtain. The PTT connection also gives CATL positioning in Thailand’s energy transition — PTT is simultaneously a major gas supplier, a renewable energy investor, and the state institution most directly exposed to the structural shift from fossil fuels to electrification.

EVE Energy, a Shenzhen-listed battery cell manufacturer, received BOI approval for EEC production — part of a broader EVE expansion across Southeast Asia targeting lithium iron phosphate (LFP) cell production for the regional market. Sunwoda 欣旺达, another Shenzhen firm specializing in battery packs and consumer electronics batteries, has similarly received BOI approval for EEC operations. These are not household names in the way BYD and CATL are, but their presence in the EEC indicates that the investment wave is reaching into second-tier supply chain depth — the kind of integration that preceded the establishment of a Japan-centered automobile ecosystem in the 1990s.

Japanese battery and component suppliers followed Japanese automotive OEMs into the Eastern Seaboard across the 1980s and 1990s, creating a supply chain network dense enough to constitute a genuine agglomeration economy — firms could locate in Chonburi or Rayong and source components, tooling, and technical labor locally. Chinese battery supply chain investment is following a similar trajectory, but compressed into a much shorter timeframe and driven partly by overcapacity at home rather than by organic export demand. CATL, BYD, and EVE are all dealing with brutal domestic margin compression as Chinese EV penetration reaches saturation. Thailand — with its BOI incentives, existing industrial estates, and proximity to ASEAN’s growing car market — offers a relief valve.

Thailand as burgeoning ASEAN data center hub

Thailand is now seeing a ramp up in data center investment. In 2025 alone, Thailand’s BOI approved 36 data center projects worth approximately US$23 billion, with roughly two-thirds concentrated in the EEC. The country is targeting 1 gigawatt of data center capacity by 2027, tripling its 2024 baseline.1 On the data center side, investment is more balanced across Chinese, Western, Japanese, and Singaporean capital. AWS, Google, and Microsoft have all made significant commitments and opened dedicated cloud regions in Thailand in the past few years. Amazon’s $5bn commitment over 15 years is the largest in absolute value, although its immediate investments have not been indicated out of this large commitment. Google opened its cloud region in January of 2026, and Microsoft announced similar intentions in early 2026.2

Whereas smaller co-location facilities had previously clustered in and around Bangkok itself, the EEC’s cheaper land, energy, and water availability makes it a natural destination for hyperscale facilities, which require large amounts of all those inputs. Bridge Data Centers, a Chinese-founded company (but with significant backing by Bain Capital), is building a large 100+Mw facility in Chonburi on a coastal mangrove forest described in the article’s opening. DayOne, the rebranded international unit of Chinese data center firm GDS, broke ground on a 1GW campus at Amata City Chonburi in March 2025. Beijing Haoyang Cloud & Data Technology purchased land for a 300MW facility at US$2.16 billion WHA Eastern Seaboard Industrial Estate 4 in Rayong in June 2025, in the same estate where Chang’an motors is building its new plant, and where AWS has already opened one of its new data centers. Galaxy Data Center (owned by Hoyinn Technologies) is planning a 1GW facility in Rayong’s Ban Chang district.

Many foreign cloud firms are partnering with local intermediaries. ST Telemedia, a Singaporean co-location DC operator, has a JV with Frasers, a division of the Thai conglomerate ThaiBev. Google and Microsoft both announced energy partnerships with Gulf Energy to supply their new facilities. True Digital, a subsidiary of the powerful CP Group, has partnerships to offer access to many of the leading cloud platforms through its data centers and has close partnerships with Huawei in particular.

What distinguishes the data center buildout spatially from the EV story is its relationship to submarine cable infrastructure. Laem Chabang Port, built with Japanese ODA in the 1980s as a container terminal, is also where several regional and international submarine cables make landfall. Google’s TalayLink cable (connecting Thailand and Australia, announced alongside its Bangkok cloud region launch in January 2026) lands there, as do older regional cables.3 Data center location in Chonburi and Rayong is determined not only by energy and water availability but by latency and connectivity: these provinces offer large serviced land, industrial-grade power, and fiber connectivity.

Global Supply Chains, Local Environmental Consequences

In one sense, the wave of investment into Thailand’s EEC is not new—it is merely the latest instance Thailand’s engagement with foreign investment in manufacturing. Today’s EEC is being remade by Chinese investment in battery and EVs, while data center investment in attracting a wider range of capital including Chinese, Western, Middle Eastern and Asian DC operators. Chinese industrial presence in the EEC spans the production of physical goods (vehicles, battery cells), digital infrastructure (compute, storage), and energy systems (grid-connected power, renewable PPAs). This is not coordination in any centralized sense — BYD, CATL, Haoyang, and DayOne are operating on independent commercial logics. But the spatial outcome of those independent decisions is a Chinese industrial footprint in the EEC that is wider and deeper than any single category of investment suggests.

The spatial consequences of this largely unregulated investment is also a continuation of earlier logics—Thai industrial estate developers ( WHA, Amata, and Rojana) acquire larger tracts of land and sell or lease to foreign investors. The scale of new facilities is visible in aerial photography of the sites—massive enclose compounds. In the case of BYD’s WHA 36 site in Rayong, their factory includes worker housing, production plants, water treatment facilities, and energy production.

The question of local benefit remains debatable. On the one hand, EV and battery ecosystems could lead to a genuinely dense cluster of related industries and spur network effects, shaping the EEC into an EV industrial base. However, numerous reports suggest much of the labor is imported—on both the higher and lower end of the value chain.

Chinese companies bring in their own labor. For the Bridge data center, its mostly Myanmar and Cambodian workers usually.”

— Somnuck Jongmeewasin, EEC Watch, May 2025

This pattern of labor importation is consistent across EV assembly and data center construction. It reflects a strategic choice to keep costs low and supply chains controlled, but it limits the local employment multiplier that BOI incentives are ostensibly designed to generate. The Thai government’s BOI negotiations with data center investors have run into exactly this tension: the Board reduced corporate tax exemptions for data centers from 10 to 8 years partly in response to arguments that the employment benefits were not commensurate with the fiscal concessions. Data center operators argue that DC investment spurs broader digital transformation, but this may hard to link directly to any one specific project and the benefits will not generally accrue directly in the communities where the facilities locate but rather in the companies that use them—and they are most likely in Bangkok itself, Singapore, or beyond.

The environmental impact of largely unregulated investment could be massive while local benefits fairly limited. The 2018 EEC Act provided legal authority for formally overriding local zoning and planning in the three provinces. The EEC Policy Committee is chaired by Thailand’s Prime Minister, and has authority to grant concessions and oversee development in the area. This, coupled with an almost total absence of environmental assessment, lack of community consultation around major facilities were features of the zone’s designation, not symptoms. They were intended to make the EEC frictionless for foreign capital. Under Japanese developmental investment, this produced agricultural land loss and water competition that farmers in Chonburi and Rayong are still living with. Under the current wave, those same dynamics are being accelerated by data centers competing with households for reservoir water, and by battery factories introducing new chemical handling risks into an already over-stressed industrial landscape.

https://www.nationthailand.com/pr-news/pr-news/40065898

https://news.microsoft.com/source/asia/2025/11/18/microsoft-announces-landmark-strategic-commitment-to-accelerate-thailands-ai-powered-growth-and-inclusive-innovation/

https://cloud.google.com/blog/products/infrastructure/talaylink-subsea-cable-to-connect-australia-and-thailand