Affordable Housing in China: Back to the Danwei?

Xiong'an is pioneering a new approach to affordable housing in China that resembles some aspects of housing in China's planned economy period. But not entirely..

The policies being deployed in Xiong’an represent some of the strongest efforts to re-link provision of housing to employment, a reversal of 30+ years of policy direction under the reform and opening, when housing was separated from the “work unit”

In his Address to the 19th Party Congress, Xi Jinping said “Houses are built to be inhabited, not for speculation.”1 This now oft-repeated slogan has come to characterize Xi’s general disapproval of the way housing has become increasingly a financialized asset in urban China, reflected in skyrocketing home prices in major Chinese cities. More recently, the real estate downturn has put a different type of pressure on Chinese cities as inventory of housing goes unfinished or unsold, and local government struggle to maintain their expenditures with land revenue from leasing to developers, which had become a major source of local budgets, in decline. Policymakers are sending mixed signals—on the one hand the real estate downturn is seen as a necessary correction to an economy that had become over-reliant on real estate. On the other, recent measures to prop up the real estate market suggest anxiety about continued drag of the property crisis on the broader economy.2 Converting empty or unsold units into affordable housing has been floated as one policy solution recently, which could significantly raise the percentage of affordable housing in some Chinese cities.3

As many of you may know, I’ve been writing extensively about Xiong’an New Area over the past couple years. Despite many people (both inside and outside of China) telling me its been a total failure, I keep following its development because its support from top leadership (i.e. Xi) has ensured it keeps receiving financing and support—and sure enough, construction is continuing apace. But while very few people even in China have any concrete idea what’s actually going on in Xiong’an, in fact a lot of the policies being trialed there will or could have implications for the rest of the country. To be sure, Xiong’an may be unrepresentative of typical cities in China and is a heavily politicized project. It may or may not represent a ‘model’, but because of its close association to the ideas and ideology of Xi himself, we can at the very least glean a sense of the ideals and intention in policies being deployed in Xiong’an. If Xiong’an is talked about as a template of high-quality development (高质量发展的国家样板), its because its intended that way—a very concrete showcase of how top leadership intends to resolve certain dilemmas facing urban and rural China. Whether these experiments succeed or are scaled up remains to be seen.

Housing is one area in which Xiong’an has been “ahead of the curve”, so to speak. The area has developed a system of affordable and subsidized housing from the very beginning of its development, and thus at the very least is worth our attention. Is it a return to the danwei 单位 era when urban residents were provided housing units from their work units?

Breaking the system of land finance?

Xiong’an has been tasked with finding alternative models of housing and land finance. Land and housing sales were halted upon the declaration of the new area in 2017 to prevent speculation. After the announcement of Xiong’an in 2017, there was indication that Xiong’an would not follow the typical “land leasing” or 土地财政 model that many Chinese cities and new areas had relied on for the better part of three decades. The head of the Shijiazhuang branch of People’s Bank of China (PBOC) wrote, “Xiongan New Area has made it clear that ‘it will not engage in large-scale land leasing or land finance, and let low housing prices become a core competitiveness of the new area,”4 I will not go into detail on land finance, which has been extensively studied in recent years, but you can find additional resources on this in the footnotes.5 Suffice it to say the term refers to the general mechanism of city & local governments selling lease rights of urban land to housing (or industrial) developers, which became a key source of local revenue in recent years—and particularly since the 2009 stimulus, using land as collateral for borrowing, typically through the formation of so-called “local government financing vehicles.”

The proclaimed “end of land finance” in Xiong’an begged an obvious question—without land sales or use of the land as collateral for borrowing and with significant subsidized rental housing, where would financing for development come from? Transitioning away from land finance meant completely rethinking not only infrastructure finance but also the system of housing and real estate development. Ni Pengfei of the Chinese Academy of Social Sciences proposed one idea: “Different from the past, there is plenty of money now, especially social funds [shehui zijin], which are abundant and have no place to invest, so we start here…by establishing various real estate development funds to attract funds from the public, the public hands over the funds for profit or public welfare companies, and these companies invest or entrust development and operation to enterprises.”6

Annual Land Leasing 土地租赁 : An annual “property tax” in all but name?

According to a former employee of an SOE housing developer who was involved in meetings of a “housing policy working group” in Xiong’an, “We had a lot of discussions early on with the government about suitable models, and obviously the Singapore model was often discussed.7 Ultimately I believe there will be a mix of housing types, some for rental, some subsidized purchase and some market rate.”8 More on this below, but first a bit about land leasing. Far from completely ending land finance or the use of land as collateral, there are new mechanisms being tried to lease land, with direct implications for housing developers. Xiong’an has experimented with different forms of “land leasing” including an annual tudi zulin 土地租赁 whereby the developer pays a fixed or variable yearly fee for the land across the entire period in which the land is leased. Huarun (CR Land) was one of the first entities to obtain land in Xiong’an via this mechanism. Plot XARC-0001 was leased to Huarun for the Green Building Exhibition Center for a 20-year period with an “annual rent” of 2.26 million RMB/ year, or an estimated total of 45 mn RMB for the entire 20 year period (1100 RMB/m2)—a low price. As a former employee of Huarun who worked in Xiong’an recounted to me, “From Huarun’s or other developer’s perspective this is good because we only have to pay a fixed proportion of the total amount, so there is less financial pressure and we are more willing to develop the land.”9 In China, land transfer fees (tudi churang jin 土地出让金) are often paid as a one-time fee to the city or LGFV up front by the developer, an infusion for city coffers but a high up-front cost for developers, incentivizing them to aim for maximum profit or demand down payments from home buyers before housing construction starts. This is a common practice that has come under scrutiny following the financial collapse of several of China’s major private homebuilders like Evergrande and Country Garden. Such an annual fixed fee “land lease” model may not be a land or property tax by name, but it more closely resembles such a tax than one-time up-front transfer payments.

A Four Tiered Housing System

An official announcement in 2023 outlined the basic contours of Xiong’an’s 4-tiered housing system, two of which are sales-type 销售型住房 and two of which are rental 租赁型住房.10

Sales:

i.) Commercial Housing 商品住房

ii.) Shared ownership housing 共有产权住

Rental:

iii.) institutional rental housing 机构租赁住房 (would refer to housing rented by specific employers for some of their employees)

iv.) insurance rental housing 保障性租赁住房 (low income rental housing)

Shared ownership housing essentially means the purchaser splits ownership with the government. This has already been tried elsewhere in China such as in Guangzhou and Shanghai. Owners can buy or sell, but there are typically limitations on this compared to fully market housing. Proportion of ownership shares may vary depending on financial resources of the buyer. It appears that relocation or 安置 (anzhi) housing for relocated villagers falls under shared ownership housing.11 Policies aim for “no less than 30%” of homes as rental units” within market housing projects.12

“What you see is what you get” and “equal access to services for renters and buyers”

Policies also call for “equal rights for renters and buyers,” such as renters being able to enjoy the same access to education, medical care, and employment” as those buying property. In many Chinese cities, property ownership or hukou status has been a source of inequity, limiting who can access services within municipalities. The policies being deployed in Xiong’an re-connect provision of housing to employment, a reversal of 30+ years of policy direction under the reform and opening, when housing was separated from work (as it had been during the 1950s planned economy and the so-called “iron rice bow” system or 铁饭碗 where housing, medical care, food, and other social services were taken care of by one’s work unit or danwei (单位).13 They also significantly increase the amount of rental and “shared property” housing.

Who gets to buy in Xiong’an?

Not just anyone can buy a house in Xiong’an. Conditions for purchasing homes in Xiong’an were unveiled last year, noting that to purchase or obtain housing in Xiong’an, residents had to meet a “3+1” policy of certain conditions:

Have to meet all of the following:

1. A formal contract signed with the relocation enterprises (or Xiongan manpower) (with the official seal of the unit)

2. No prior house in the new area

3. The first and second type of relocation enterprises have paid social security or taxes in the new area for one month, and the third type of relocation enterprises have paid social security or taxes in the new area for more than one year.

All three of the above points must be met, and one of the following options can be met:

Beijing hukou

Points-based settlement in the new area

Xiongcai card (雄才卡)-see below

Talent certificate issued by the unit with a bachelor's degree or above

Five-year social security in the new area

The Xiongcai Card is a special card issued at 3 different levels according to points given for meeting certain qualifications or educational training.14 This card will apparently offer certain benefits like discounts for city services such as transport, utilities, etc. In this way, housing policies in Xiong’an are re-connecting housing back to employment, not entirely akin to the Maoist Danwei system, but a shift away from commercialized form of housing that gradually separated housing from employment during the 1980s and early 1990s when China’s housing market begun in earnest.

There are also limits on sales even for commercial housing—which can be sold after 5 years, and shared ownership housing can be converted into commercial housing after 5 years.

Commercial Housing

The first commercial housing project to open for sales was the China Dream City or 华望城 development in the Eastern part of Rongdong District, a project of Xiong’an Group. There are even freestanding “villas” or 别墅 available here. One of the first commercial projects to be completed in the Qidong Area (the eventual CBD of Xiong’an) is China Communications Construction “Qiyuan” 启园 development, located in a favorable location across from Shijia Hutong Primary School and Beijing Fourth Middle School. To take Qiyuan as an example, out of a total of 1775 units, 306 will be commercial units (商品住房), 522 will be publicly owned (共有产权住), 604 will be “repurchased by the government” and 342 units would be rental units provided to employees of enterprises (See Figure). So even in a development built by a commercial developer there is a mix of these four different types of housing mentioned above, which is not typical for recent Chinese commercial housing developments. Xiong’an has implemented a range of other housing policies, including forbidding the “pre-sale” of housing (developers in China often required down payments before housing construction starts).15

Relocation housing 安置房 is being provided to villagers whose homes were demolished to make way for the city—the Rongdong District, which was the first area of Xiong’an to be completed, comprises mostly resettlement housing for around 170,000 people. Many villages in the area were completely demolished to make way for Xiong’an. In this way, Xiong’an began as a large-scale rural resettlement project—a tactic for “reducing extreme poverty” that has been deployed in many of China’s remote mountainous areas, with mixed results. A petition center apparently was set up in the early years of Xiong’an’s construction specifically to accommodate the flood of petitioners of villagers unhappy with the terms of compensation, but an employee I spoke with estimated over 60% of the villagers were ultimately satisfied with the terms of compensation. Some I spoke to noted how villagers received far less than those whose houses were demolished in nearby urban areas of Baoding.

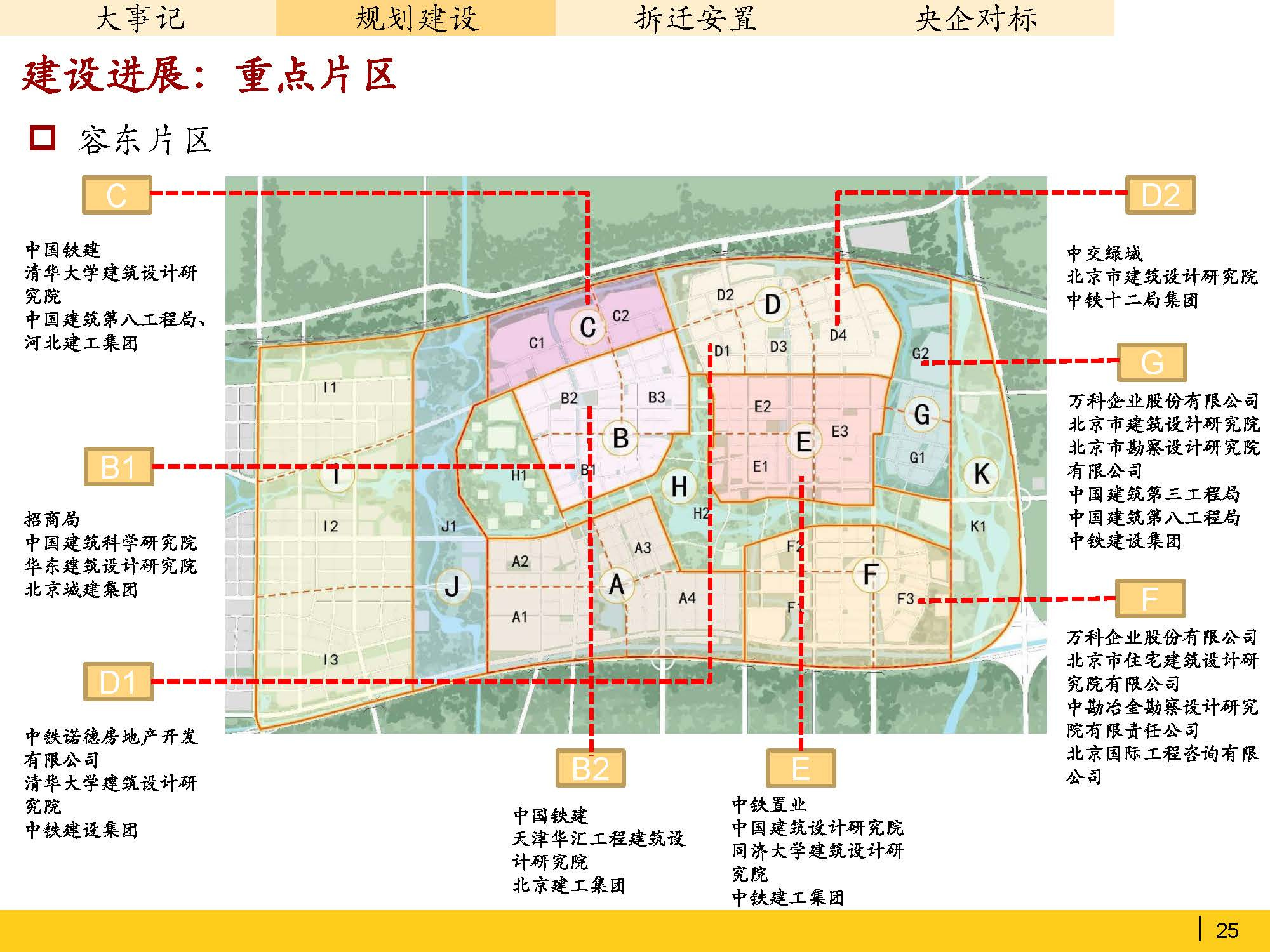

The developers building housing in Rongdong included China Merchants (Zhaoshang Ju 招商局), China Rail Construction 中铁建, China Communications 中交, CR Land (Huarun 华润) and Shenzen-based Vanke 万科. According to CR Land, a large SOE developer working in Xiong’an, standards for resettlement homes would be 50 sq meter apartments, and compensation given at 7,000 RMB/sq meter or (350,000 yuan), and a 50% subsidy of property and elevator fees for 5 years.16 So-called resettlement homes can be sold back to the government, thus reverting to shared-housing, but only after 5 years. This doesn’t seem to have prevented many villagers to rent out their units online for extra income (see below). As one taxi driver told me, “people are just sitting around in their houses with nothing to do.”

Where does housing fit in the overall financing of Xiong’an?

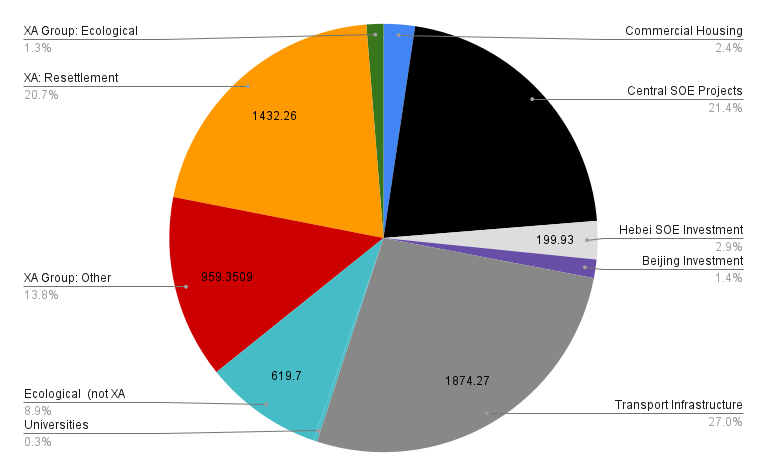

If fewer housing units are being sold at market prices, how will housing be financed? This is a question with direct implications for Xiong’an’s overall financing model. Based on extensive collection of data on nearly all of the project financing in Xiong’an, I was able to account for most of the 6900亿元(690 Bn RMB or $96 Bn) publicly reported project investment in Xiong’an up through the end of 2023).17 For most of the “resettlement housing projects” in Rongdong District, provincial bond support accounts for only a small percentage of each project, while investment by developers is expected to account for the rest. According to a source who worked for one of these developers, the Xiong’an Government would typically re-purchase the housing from the developers, after the completion of the projects. Repayment of the bonds is also supposed to draw on land revenue in other parts of Xiong’an, such as in Qidong District, the main CBD. Funding for the construction of Rongdong Area came from Hebei Province-issued bonds, alongside investment from developers themselves. The repayment of these bonds was expected to come from “land leasing, transfer, and other income generated in the communities.”18 A bond prospectus estimated that for a group of these projects, income over the duration of the bond would be 61 bn Yuan, from an initial bond value of 240 bn.”19 For one of the resettlement projects the overall investment cost would be 9.2 bn, and using a bond of around 650 million RMB would be repaid over 30 years at a total of around 1.4 bn including principal and interest. This amount would be “covered” with 2bn in income generated from land leasing in designated plots of land in Xiong’an’s core commercial area Qidong District.20

While Xi criticized the financialization of housing, the “Xiong’an model” appears in some cases to experiment with an even greater degree of financialization in the form of real-estate investment trusts (REITS), as well as investment in housing by greater diversity of SOE and some private investors. Proposals for REITs + PPP to finance public rental housing construction in Xiong’an involves the government creating a real estate trust company that will set up a REIT to receive investment. Then a project company will build housing—this company will receive capital from REITs, and the property management companies will pay back REIT investors through long-term rental income and other fees.21

While the housing system continues to take shape in Xiong’an, we can see the contours of a mixed system featuring both commercial, rental, and shared housing. In some ways, the system is a sort of compromise—not entirely the Singapore model, but incorporating aspects of it. Much of Singapore’s public housing are units built by HDB and then sold (or leased for 99 years to owners), but there is also substantial rental housing. However, the large amount of housing owned or rented directly by employers is quite distinct from Singapore and suggests the central enterprises relocating to Xiong’an will play a large role in housing provision for employees. This is even a selling point designed to attract young people perhaps put off by the high costs of housing in China’s first tier cities.

A subsequent post will explore in more detail the overall system of financing in Xiong’an New Area!

https://www.bloomberg.com/news/articles/2017-10-18/xi-renews-call-housing-should-be-for-living-in-not-speculation

https://www.bloomberg.com/news/articles/2024-05-27/shanghai-cuts-home-downpayment-as-easing-spreads-to-big-cities?sref=uccUiNCE&embedded-checkout=true

https://www.wsj.com/world/china/china-real-estate-crisis-state-housing-656c5093

[1] Chen, Jianhua (2018) Zhongguo Jinrong (China Finance) “Xiong’an xinqu jinrong dongneng dingwei” the position of Xiong’an’s finance functions” 《中国金融》2018年 第7期 | 陈建华 中国人民银行石家庄中心支行

Embedded Power: Chinese Government and Economic Development by 兰小欢 Lan Xiaohuan, Associate Professor, School of Economics, Fudan University

[1] Ni, Pengfei (2017) Xiong’an Xinqu: Zhongguo chengshi fazhan xin moshi de shiyan “Xiong’an New Area: An experiment of a new model of China’s urban development” in Think Tank Reports on Xiong’an (Series 1).

The “Singapore model” of public housing actually entails 80% of Singaporeans living in government-built houses (through Housing Development Board or HDB)—but many of these residents own their homes through an arrangement where they draw down their savings acccounts (in the Central Provident Fund) to purchase subsidized units. China also has something similar called 公积金 essentially forced housing saving accounts. But since the 1990s, most housing stock has been delivered by private developers while government-built low income housing remains an option for lower income groups. Also see: https://www.nytimes.com/2024/05/24/world/asia/singapore-public-housing-program.html

Interview with former employee of CR Land Xiong’an (2022)

Ibid

https://www.thepaper.cn/newsDetail_forward_26730545

http://www.xiongan.gov.cn/2023-09/19/c_1212269993.htm

http://www.news.cn/fortune/2023-09/21/c_1129874192.htm

Bray, David. Social Space and Governance in Urban China: The Danwei System from Origins to Reform. 1 edition. Stanford, Calif: Stanford University Press, 2005.

https://m.thepaper.cn/newsDetail_forward_20659060

https://www.chinadaily.com.cn/a/202309/20/WS650ac801a310d2dce4bb6cb0.html#:~:text=Xiong'an%20has%20implemented%20supporting,renting%20apartments%20in%20Xiong'an.

CR Land Internal Document

A dataset on all publicly announced projects in Xiong’an was compiled by scraping press releases, news articles and government and central enterprise websites for “total investment” figures of each project, where available. Information on bank financing was gleaned from news reports, press releases, bond prospectuses and company annual reports. Information on Hebei provincial bonds was obtained from database CELMA and bond prospectus reports from credit rating agencies.

Shanghai Brilliance Credit Rating (2019) “Hebei Government Xiong’an New Area Construction Bond Credit Rating Report”

Ibid.

Rongdong District B1 Relocation Construction Project Local Government Bond Project Document

Li et al (Hebei Finance (2022, 1) “PPP+REITs”模式支持雄安新区公租房建设的应用研究”

Thank you! More to come :-)

Thank you so much for the deep dive! I've been intermittently following the Xiong'an New Area project over the past 6 years and really appreciate it. Fascinating stuff.